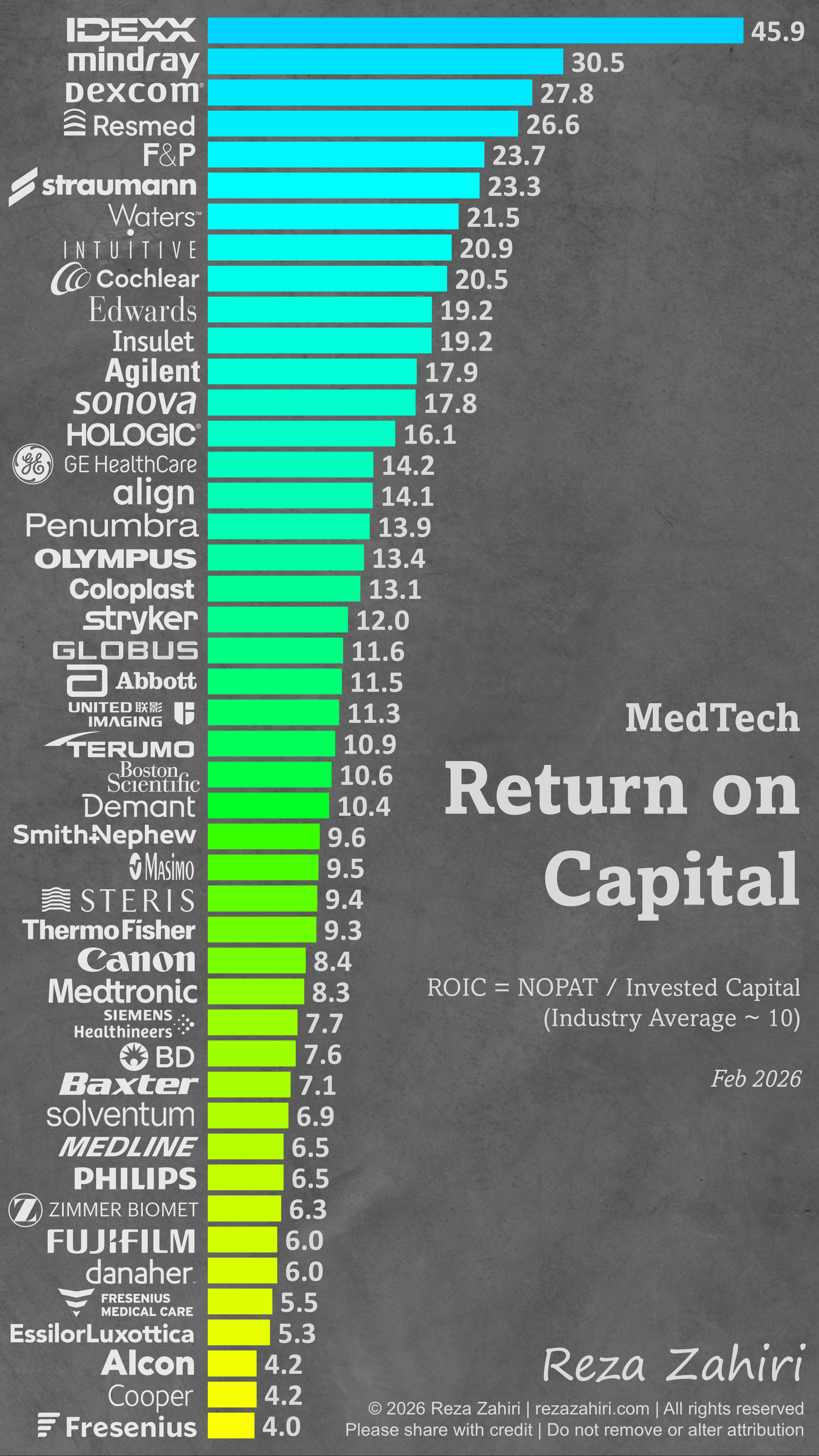

Return On Capital

Return on Invested Capital (ROIC) is one of the most widely used metrics for assessing how effectively a company is being run. At its core, ROIC measures how efficiently management converts invested capital (both debt and equity) into operating profits.

What makes ROIC especially powerful is its ability to cut through the noise. Unlike revenue growth or earnings, ROIC forces discipline around Capital allocation, Operational efficiency, M&A quality (did the deal create value?), and long-term economic moat.

In many ways, ROIC is a scoreboard for management quality. For example, revenue growth can be achieved through a major acquisition, but that growth does not automatically translate into value creation. If the combined company with the combined invested capital generates proportionally less operating profit, ROIC declines despite higher reported revenue, signaling value destruction.

Here’s a look at ROIC across the MedTech industry. The average is roughly 10%, broadly in line with the S&P 500, but the range is wide.

Limitations of ROIC

Like any metric, ROIC has its limitations:

Asset-light models look “better” by default.

When applied at the company level, it can obscure the performance of individual business units.

High-growth companies can look weak early, before profits fully materialize.

Share buybacks, which reduce equity and can inflate ROIC without improving the business.

Can be temporarily boosted by underinvestment, which hurts the outlook.

The Takeaway

ROIC isn’t perfect, but it remains one of the most effective tools for distinguishing "value-creating growth" from "capital-consuming growth". If you want a clearer view of an organization’s long-term performance, ROIC and its history deserve a permanent seat at the table.